Notice: Function wp_maybe_inline_styles was called incorrectly. Unable to read the "path" key with value "https://blog.iiasa.ac.at/wp-content/plugins/jetpack/_inc/build/subscriptions/subscriptions.min.css" for stylesheet "jetpack-subscriptions". Please see Debugging in WordPress for more information. (This message was added in version 7.0.0.) in /opt/wpprojects.iiasa.ac.at/wordpress/wp-includes/functions.php on line 6170

By Dilek Yildiz, Wittgenstein Center for Demography and Global Human Capital (IIASA, VID/ÖAW and WU), Vienna Institute of Demography, Austrian Academy of Sciences, International Institute for Applied Systems Analysis

Social media offers a promising source of data for social science research that could provide insights into attitudes, behavior, social linkages and interactions between individuals. As of the third quarter of 2017, Twitter alone had on average 330 million active users per month. The magnitude and the richness of this data attract social scientists working in many different fields with topics studied ranging from extracting quantitative measures such as migration and unemployment, to more qualitative work such as looking at the footprint of second demographic transition (i.e., the shift from high to low fertility) and gender revolution. Although, the use of social media data for scientific research has increased rapidly in recent years, several questions remain unanswered. In a recent publication with Jo Munson, Agnese Vitali and Ramine Tinati from the University of Southampton, and Jennifer Holland from Erasmus University, Rotterdam, we investigated to what extent findings obtained with social media data are generalizable to broader populations, and what constitutes best practice for estimating demographic information from Twitter data.

A key issue when using this data source is that a sample selected from a social media platform differs from a sample used in standard statistical analysis. Usually, a sample is randomly selected according to a survey design so that information gathered from this sample can be used to make inferences about a general population (e.g., people living in Austria). However, despite the huge number of users, the information gathered from Twitter and the estimates produced are subject to bias due to its non-random, non-representative nature. Consistent with previous research conducted in the United States, we found that Twitter users are more likely than the general population to be young and male, and that Twitter penetration is highest in urban areas. In addition, the demographic characteristics of users, such as age and gender, are not always readily available. Consequently, despite its potential, deriving the demographic characteristics of social media users and dealing with the non-random, non-representative populations from which they are drawn represent challenges for social scientists.

Although previous research has explored methods for conducting demographic research using non-representative internet data, few studies mention or account for the bias and measurement error inherent in social media data. To fill this gap, we investigated best practice for estimating demographic information from Twitter users, and then attempted to reduce selection bias by calibrating the non-representative sample of Twitter users with a more reliable source.

We gathered information from 979,992 geo-located Tweets sent by 22,356 unique users in South-East England and estimated their demographic characteristics using the crowd-sourcing platform CrowdFlower and the image-recognition software Face++. Our results show that CrowdFlower estimates age more accurately than Face++, while both tools are highly reliable for estimating the sex of Twitter users.

To evaluate and reduce the selection bias, we ran a series of models and calibrated the non-representative sample of Twitter users with mid-year population estimates for South-East England from the UK Office of National Statistics. We then corrected the bias in age-, sex-, and location-specific population counts. This bias correction exercise shows promise for unbiased inference when using social media data and can be used to further reduce selection bias by including other sociodemographic variables of social media users such as ethnicity. By extending the modeling framework slightly to include an additional variable, which is only available through social media data, it is also possible to make unbiased inferences for broader populations by, for example, extracting the variable of interest from Tweets via text mining. Lastly, our methodology lends itself for use in the calculation of sample weights for Twitter users or Tweets. This means that a Twitter sample can be treated as an individual-level dataset for micro-level analysis (e.g., for measuring associations between variables obtained from Twitter data).

Reference:

Yildiz, D., Munson, J., Vitali, A., Tinati, R. and Holland, J.A. (2017). Using Twitter data for demographic research, Demographic Research, 37 (46): 1477-1514. doi: 10.4054/DemRes.2017.37.46

Note: This article gives the views of the author, and not the position of the Nexus blog, nor of the International Institute for Applied Systems Analysis.

By Isela-Elizabeth Tellez-Leon, IIASA-CONACYT postdoc in the Advanced Systems Analysis, Evolution and Ecology, and Risk and Resilience programs.

The rise of foreign investment in emerging economies after the global financial crisis of 2008-2009 has renewed interest in what drives such investment. My colleague at the Central Bank of Mexico and I examined the determinants of foreign investment, known as capital flows, into Mexico in 1995-2015, a period characterized by a free-floating exchange rate, that is, the authorities did not set an exchange rate.

Our research has useful findings for the design of economic policies because it provides measures that authorities can take to direct proper functioning of the economy. It also contributes to improved understanding of what influences capital flows into Mexico. We analyzed the determinants of each type of foreign investment separately, because different financial flows respond differently to the various external and internal factors. Mexico is an interesting case study because it experienced a large volume of capital investment after the commercial opening in the 1990s and more recently in the aftermath of the 2008-2009 financial crisis, as international investors were searching for high yields and security. In addition, the trading volume of Mexican government securities is one of the highest among emerging markets.

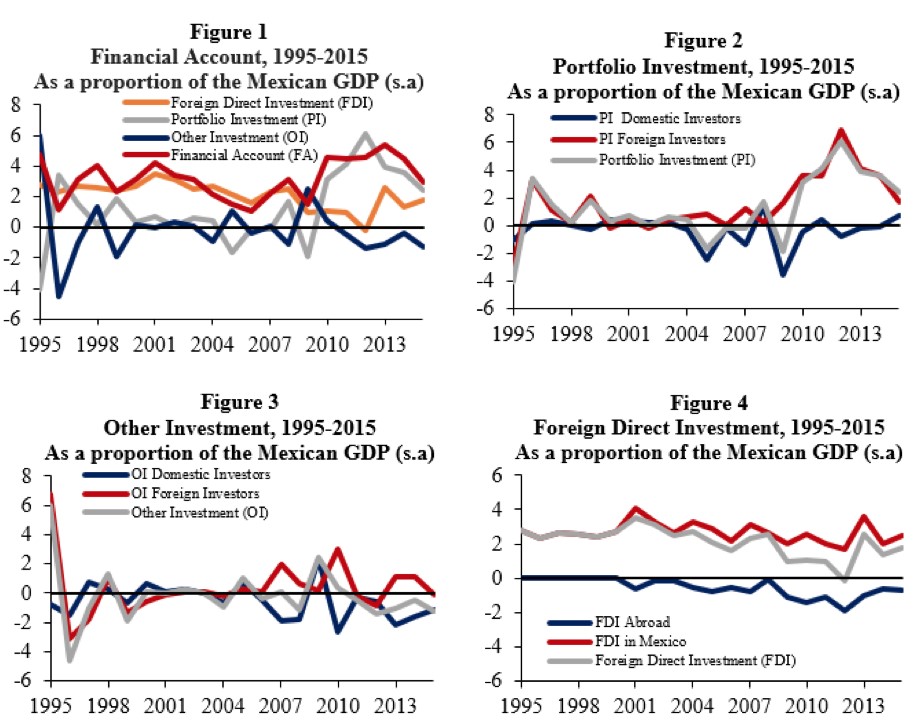

Capital flows are incorporated into financial accounts where foreign transactions are noted—including investments by foreign residents into Mexican public and private sector securities and by domestic residents in foreign securities. Mexico’s financial accounts (Figure 1) are composed of the following three components: portfolio investment (in terms of liquidity—i.e., the extent to which a market allows assets to be bought and sold at stable prices—this is a short-term investment, Figure 2), other investment (Figure 3), and foreign direct investment (in terms of liquidity this is a long-term investment, Figure 4).

The financial account is divided into three main areas: foreign direct investment (FDI), portfolio investment (PI) and other investment (OI). Figure 1 shows the net flows of foreign investment. Figure 2 displays portfolio investment (PI) and its components of domestic and foreign investors. Figure 3 and 4 show OI and FDI split into their different components. The figures show moving averages over 4 quarters adjusted for seasonality. Source: Elizabeth Tellez and the Central Bank of Mexico.

Portfolio and other investments tend to leave and enter a country quicker than foreign direct investment; thus, they are likely to respond faster to shocks. In particular, portfolio investment by foreign agents might have a different response compared to portfolio investment by domestic agents. For example, if foreign investors have timely information about the external economic conditions, they will likely respond faster to foreign shocks.

In general, foreign investment has an impact on developing economies in at least two ways. On the one hand, international borrowing allows a country to increase investment in the private sector, without sacrificing consumption. On the other hand, large foreign investment flows may be followed by increases in the prices of goods and services because of the strength of the exchange rate. In turn, this increases purchases of foreign products (imports), but exports decrease. In this way, a country’s foreign trade may become more vulnerable to external shocks and reversals of foreign investment.

To analyze what determines capital flows in the short and medium term for Mexico, we used an econometric model known as Vector Autoregression. This model allows us to examine the impacts of different shocks on capital flows. We studied two sets of factors that can encourage investors to shift resources to emerging markets. The first set considers external shocks (push factors), which are beyond the control of developing countries, such as foreign interest rates or economic activity in advanced countries.

The push factors we examined were global risk, US liquidity, US GDP, and US interest rates. The second set of factors are the prevailing economic conditions in the emerging economy (pull factors). For these we considered Mexican GDP, interest rates, inflation, and exchange rates.

One of our main findings is that investors are risk averse and prefer to invest abroad when foreign interest rates are higher. Portfolio investment (PI) and other investment (OI) seem more responsive to short-term shocks than foreign direct investment (FDI), possibly because they tend to be more liquid than FDI. We also found that domestic conditions play a role in explaining capital flows. For instance, we found that higher GDP growth leads to higher portfolio investment, while higher interest rates and lower inflation generate higher inflows of other investment. Our work underlines the benefits of separately analyzing the components of capital flows. For instance, a shock to the federal funds rate has important effects on portfolio investment in public-sector securities by foreign residents. This is because public securities are the closest substitutes to US government bonds found in the Mexican financial market.

By Hannu Halinen, special advisor to the director general and CEO of IIASA

The Harpa Center at Reykjavik Harbor is the scene for one of the biggest annual gatherings of Arctic researchers, politicians, business representatives, indigenous peoples, nongovernmental organizations, and students; the Arctic Circle Assembly. Under the roof of this architectural landmark some two thousand participants spend a long weekend discussing a multitude of Arctic issues. This year there was an added attraction next door to the Harpa Centre: Finland, as a part of her 100 year independence celebration, had brought the multipurpose ice breaker “Nordica” to Reykjavik. A number of the assembly events were held on board the vessel, and everybody—both assembly participants and Icelanders— wanted to take the rare chance to see this impressive ship. The sea around Iceland is ice-free thanks to the Gulf Stream; hence no need for ice breakers.

The official assembly program consisted of a few high-level plenary sessions and many parallel break-out sessions. IIASA and the Arctic Futures Initiative (AFI) were introduced at the assembly in 2015, and I was busy at that time introducing Pavel and Anni to my Arctic colleagues. I can safely say that the time then was effectively used to build and strengthen the network between IIASA and Arctic actors.

By 2017 we were many steps ahead, as AFI has become a well-known Arctic endeavor and launching the collaboration between IIASA and the Arctic Circle was a major development. I have had the privilege to be associated with AFI over three years now, and one of the challenges for me all along has been to explain to those interested what AFI is about. Because my background is as a diplomat and a civil servant, the concept of a research project has been something new to me—and to many other decision makers and business leaders as well.

Everybody is asking what new angle can the AFI bring, and what’s in it for me? The collaboration between the Arctic Circle and AFI is a prime example on how to respond to the question. A wealth of insights and information is provided in hundreds of interventions at the assembly. What is missing is the analysis, follow up and possible implementation of the inputs during the Assembly. Here AFI can give the crucial assistance needed through systems thinking, models, and scenarios.

Two years ago we had one break-out session at the assembly. This year AFI was presented by Pavel and the former President of Iceland Olafur Grimsson at a plenary, as well as in three well-attended break-out sessions covering how systems analysis perspective can be invaluable to the challenges and opportunities that the Arctic faces; how the opening of the Northern sea route might impact global trade, and Arctic fisheries assessments.

The network is now largely built, the project development phase is coming to the end, and the focus of the work is shifting to carry out the project itself. But many issues still need to be tackled: who will organize and carry out the work, for example, how to solve the funding issues, and so on. I have believed in this project from the beginning. With wise and decisive action the remaining questions can be solved.

Note: This article gives the views of the author, and not the position of the Nexus blog, nor of the International Institute for Applied Systems Analysis.

By Peter Havlik, senior economist and former deputy director at the Vienna Institute for International Economic Studies.

Foreign direct investment (FDI) has been the main driver of restructuring and modernisation of many countries’ economies. In Central and Eastern Europe, FDI has been instrumental in both privatisations of state-owned enterprises and in launching new investment projects. FDI flows in manufacturing have created modern, competitive, export-oriented industries and generated export revenues. However, FDI flowing into the services sectors (including finance and insurance but especially retail trade and real estate) have been more controversial since they boost import demand rather than create new export opportunities.

Global FDI flows are highly volatile and there is no straightforward explanation for such fluctuations. In 2016, FDI to Russia went up sharply, partly because of a single large transaction related to the oil company Rosneft; flows to Kazakhstan recovered as well. FDI flow into Ukraine also increased in 2016, primarily due to bank recapitalisations (reorganization of how a corporation finances its assets) and the privatisation of some companies with the participation of institutional investors such as the European Bank for Reconstruction and Development. FDI flows to Georgia were relatively high in 2014-2016, presumably thanks to the implementation of the Deep and Comprehensive Free Trade Areas (DCFTA), three free trade areas established between the EU, and Georgia, Moldova, and Ukraine. A similar trend, albeit at a much smaller scale, was observed in Moldova.

DCFTA countries have been laggards with respect to attracting FDI, largely due to ‘frozen’ conflicts over disputed territories and a poor investment climate in general. Moreover, FDI in the DCFTA countries, similarly to Russia, have a skewed geographic origin: in Ukraine, for example, more than 30% of FDI stocks originate in Cyprus; the share of FDI from Western Europe was just 36% of total FDI stocks in 2016. The extremely high shares of Cyprus and other offshore destinations indicate that this kind of FDI most likely just represents a recycling of domestic capital flight— when assets or money rapidly flow out of a country—and possibly also tax evasion. One can probably safely assume that this kind of FDI is also not particularly conducive to upgrading and modernising the economy. Progress towards institutional reforms in general would therefore instead result in diminishing the shares of FDI that originates from offshore.

The experience of EU countries in Central and Eastern Europe (EU CEEs) indicates that FDI inflows have significantly contributed to the modernisation and restructuring of their economies (about 80% of FDI there originates from Western Europe in contrast to less than 40% in Russia and Ukraine). FDI in the manufacturing industry, business services such as IT, software development, and logistics, has been especially beneficial. Such investments have been particularly welcome as they help to establish competitive export-oriented industries (the successful German-CEE automotive cluster is a case in point). After EU accession, foreign investors have to be treated as domestic ones. Recently, though, a renewed economic nationalism in some countries, such as in Hungary and Poland, has resulted in selective treatment of investors by economic sectors, causing a de facto restriction of foreign investment in banking, trade, etc.

However, it is not just the volume of the registered FDI and its origin that matter; its sectoral composition, investors’ motives, and other FDI structural and ‘quality’ characteristics are also important. In EU CEEs, the bulk of FDI has been concentrated in manufacturing, trade, and financial services: each of these three broad sectors account for about 20-30% of total FDI stocks. In this respect, the DCFTA countries are not very different from Hungary, Poland, Romania, or Slovakia. As far as Eurasian Economic Union countries are concerned, most FDI has been concentrated in energy and mining sectors (especially in Kazakhstan and Russia). In Moldova, Ukraine, and Romania, there are some (small) foreign investments in agriculture. The energy sector is an important FDI target in Georgia, Moldova, and Romania (there are no comparable data for Belarus).

How to explain the huge differences in various FDI structural characteristics across individual transition countries? A number of factors definitely play a role: geography, size of the country, resource endowments, costs and skills of labour, government FDI policies and the investment climate in general. According to the latest World Bank Ease of Doing Business survey for 2018 (published on 31 October 2017 and registering big shifts in ranking scores), Eurasian Economic Union and DCFTA countries received the following ranking (out of 190 countries surveyed): Georgia (9), Poland (27), Russian Federation (35), Kazakhstan (36), Belarus (38), Slovakia (39), Moldova (44), Romania (45), Armenia (47), Hungary (48), Azerbaijan (57), Ukraine (76) and Kyrgyzstan (77). Russian Federation, Kazakhstan, Belarus and Georgia were among the top 10 countries which have managed to improve their ranking recently.

In conclusion, the analysis from the forthcoming IIASA Fast Track FDI study implies that Eurasian Economic Union and DCFTA countries have not been particularly attractive for foreign investors; and if ‘round-trip’ inflows from offshore are excluded this issue is even more evident. This goes a long way to explaining why restructuring in the region has stalled. This pattern can change only with marked improvements in the domestic regulatory environments and investment climates. FDI inflows should also be promoted by pro-active government policies (at national and regional levels) which focus on attracting FDI in manufacturing and business services in order to assist restructuring and modernization.

Note: This article gives the views of the author, and not the position of the Nexus blog, nor of the International Institute for Applied Systems Analysis.

By Nemi Vora, participant of the IIASA Young Scientists Summer Program (YSSP) 2017 and PhD student at the University of Pittsburgh.

“Was it worth the flight?” asked my fellow alumna of the YSSP Karen Umansky, at the end of our first day of attending the World Science Forum in Jordan. The total journey from the USA to Jordan had taken 20 hours, layovers included. She was well aware of my travel anxiety, fear of immigration officials (an Indian passport doesn’t always make things easy), and fear of traveling alone on a militarized Dead Sea road at night (you can see the west bank on the other side). I had spammed her every day about it.

I didn’t have an answer; the panels I attended did not focus on anything new. We were all aware of issues: digitization without destruction, women in science, support for emerging scientists, meeting the sustainable development goals, and so on. However, every conference has a different key to unlock its potential and Jan Marco Müller, head of the IIASA directorate office and another recipient of my daily email spam, informed me that it was not the panels, but the corridor conversations that mattered here.

I soon found out that it was not just the corridors, but even the brief conversations in shuttles where the conference happened. I met a program manager for the US National Science Foundation who told me about research work on the food-energy-water nexus that they funded for the Nile, an area similar to my thesis. I met a regional director of UNESCO and a science minister from Colombia, who together set up new Africa-Latin America project partnerships during the shuttle ride.

One important part of each conversation was the significance of the place I was in, something I had previously missed completely. The ability of this small country, surrounded by conflict zones on each side, to arrange for such a large gathering of this kind, bringing together opponents and allies alike, and to take a stand for enabling peace through science, was remarkable.

True, the issues were not new, but the context was much more specific to the needs of a conflict-ridden world. For instance, discussing how to provide access to digital resources such as open data for policymaking or scientific journals for all the countries, promoting the achievements of Arab women scientists and those of the other developing regions amidst cultural and economic hardships, and fostering innovation in emerging scholars in the developing world where lack of resources was part of academic life.

Jordan also showcased the recently established SESAME facility: the Middle East’s first international science research center, a joint venture of a group of middle eastern countries, otherwise engaged in political conflicts. IIASA was representing a unique position here: originally founded as the bridge between East-West scientific collaboration during the Cold War, it served as an example, along with the fledgling SESAME, that geo-political boundaries did not hinder science and that such projects could be successful. Despite political tensions in individual countries, and having a passport that would not allow you to visit your colleague’s country, you could still work side-by side—a feat that SESAME scientists achieve every day.

As YSSPers, our goal was to talk about the benefits of global mentorship and how that could be leveraged to address the uneven distribution of resources. All of us came from different backgrounds: there was An Ha Truong from Vietnam, an energy economist studying optimization of biomass for coal power plants, there was Karen, the social scientist from Israel, studying emerging neo-Nazism in Europe, and then there was me—representing the USA and India as an environmental engineer.

Our co-panelists from the Berkeley Global Science Institute, also of diverse backgrounds, were engaged in setting up labs across the world, providing resources and mentorship to graduate students. While we had a lively session discussing our personal experiences, it wasn’t what we had to say but the session questions that struck a chord with us. The presence of conflicts add another layer of complexity to the already murky path of academia: how do you keep young scholars motivated to stay in the lab and work in a country threatened by war? How do you compete in cutting-edge science research when resources are scarce? How do you engage in public-private partnerships when your work may be more theoretical than applied?

We need to collaborate more, provide access to the data and codes we use to carry out reproducible research, attempt to publish in open access platforms whenever feasible, and support our fellow scientists irrespective of their location or positions. This way, we would inch closer to solving some of these issues. Six months ago at IIASA, the HRH Sumaya bint El Hassan, co-chair of the World Science Forum, had asked me, “How do you eat an elephant?” Being a vegetarian, I couldn’t imagine ever eating one and I very naively told her so. On my way back from Jordan, with another long journey ahead of me, I realized the significance of her words: you eat it little by little.

Follow Nemi on twitter: @NemiVora

This article gives the views of the author, and not the position of the Nexus blog, nor of the International Institute for Applied Systems Analysis.

Notice: Function wp_maybe_inline_styles was called incorrectly. Unable to read the "path" key with value "https://blog.iiasa.ac.at/wp-content/plugins/jetpack/_inc/build/subscriptions/subscriptions.min.css" for stylesheet "jetpack-subscriptions". Please see Debugging in WordPress for more information. (This message was added in version 7.0.0.) in /opt/wpprojects.iiasa.ac.at/wordpress/wp-includes/functions.php on line 6170

You must be logged in to post a comment.